Renewable Thermal Heating: Lessons from Scandinavia

How financial innovation and regional cooperation can cultivate a New England market for renewable thermal technologies.

The built environment – essential to a low carbon future

Connecticut is one of several New England states that hold lofty ambitions for reducing greenhouse gas (GHG) emissions by 2050. Achieving this low-carbon future will require, among other things, a transformation of the built environment, which is responsible for around 12.6 million tons of GHG emissions every year due to demand for hot water and space heating and cooling.

Renewable Thermal Technologies (RTTs)[1], now gaining attention as a valuable emission reduction tool, represent mature technologies in an immature New England market; presently, the market is typified by high upfront costs, lack of customer awareness and trust, a weak network of suppliers, and a thin competence base. Fortunately, the region has a few building blocks that can be turned into key factors for the successful deployment of RTTs. In particular, New England can work regionally and can build on existing financial innovations.

Scandinavia, which has developed a robust RTTs market and is similar to New England in its size and the severity of its winters, offers an interesting point of comparison. Each Scandinavian country pursued a different path to RTTs deployment, but the region—and Norway in particular—provides useful takeaways for building a New England market.

Scandinavia’s various approaches

A region of 21 million people, Scandinavia has densely populated urban areas, like Copenhagen, Stockholm, and Oslo, as well as vast sparsely populated countryside. Winters are cold, as in New England (though they are longer). Electricity demand poses a challenge in dry years with cold winters due to dependence on hydroelectric power. Scandinavian countries, just like New England, also share a wholesale electricity market, though the countries have very different energy systems—ranging from Norway’s dependence on electric resistance heating to the widespread use of biomass in Sweden and district heating in Denmark. Energy sources vary, too: Norway produces 99 percent of its electricity from hydro, Sweden 50 percent from nuclear while Denmark generates 41 percent of its electricity from fossil fuels and 42 percent from wind power.

All three countries have committed to contribute to the 2050 GHG emission reduction targets of the European Union. With the exception of a joint green electricity certificate market between Norway and Sweden, each country has taken a different approach to achieving these targets. Thus, market conditions for renewable heat differ from country to country. With abundant access to cheap hydro power, Norway started diversifying into thermal technologies at a later point, making it an interesting example of a recent market development that targeted RTTs.

Transforming the Norwegian heating market

The world’s first district energy system, which used steam to carry heat, was introduced in the U.S. in the 1880s. District energy systems provide heating and cooling to buildings and processes through networks of hot and cold water pipes and today are transitioning to a fourth generation. This new generation of smart thermal energy grids will tackle the challenges of heat supply to energy efficient buildings and the integration of low-temperature heat sources, such as surplus heat from industrial processes and data centers.

Being a latecomer in district energy allowed Norway to begin with third- and fourth-generation thermal loops that incorporated a high share of renewable energy sources. The district energy grid doubled from 2008 to 2015, investments accounted for 190 million dollar in 2015, and district energy represented an estimated 10 percent of the heating demand of buildings. Although waste incineration dominates as a source of district energy, local resources such as seawater, ambient ground heat, residual wood waste, industrial waste heat, and solar thermal are exploited, while oil and gas furnaces cover peak demand and serve as backup.

Important elements of such extensive development of a district energy infrastructure included:

- Investment support to reduce upfront cost and risk in the development phase.

- Supportive regulations such as a ban on fuel oil boilers in new buildings combined with a required minimum share of renewable thermal energy.

- Price regulation and mandatory connection for certain categories of buildings near district energy networks.

- Good timing.

Small-scale thermal loops that connect a limited number of buildings together through thermal infrastructure have also been established based on locally available resources. These thermal loops typically deliver to universities, military bases, hospitals, and clustered municipal buildings. Different ownership structures (like third-party ownership) and novel business models (like energy performance contracts) have supported this development.

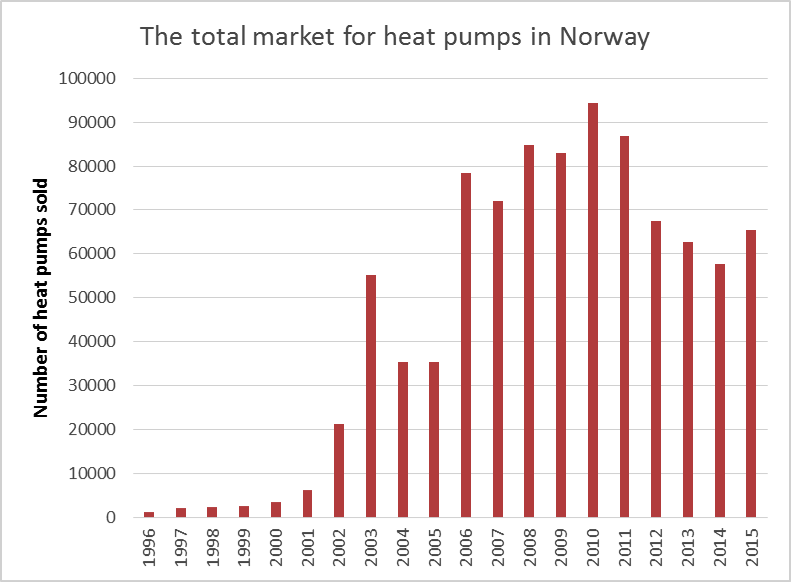

In 2000, heat pumps were a technology with low customer awareness in Norway; by the end of 2015, total installations reached 900,000—striking for a country with a population of 5.1 million inhabitants. The number of annual heat pump installations was ten-times higher in 2015 than it was in 2000. What elements contributed to this development?

In the beginning of the millennium, Norway experienced a series of cold and dry winters and electricity prices spiked. Media attention on this issue, as well as on investment grants for renewable thermal technologies, made customers aware of the heat pump as one technology that can reduce and stabilize costs. As the market developed and matured, grants for thermal technologies were slowly removed; the market for air-to-air heat pumps was ready to prosper without grants. At the same time, regulations helped push renewable thermal technologies (and heat pumps in particular):

- Building code banned oil boilers in new buildings and required a certain share of renewable thermal energy, sending strong signals that fuel oil for heating was to be phased out.

- The EU Building Energy Directive requires all buildings that are sold or rented to post an Energy Performance Certificate, allowing customers to compare the energy performance of buildings. Integrated thermal technologies benefited from this.

Innovators across the value chain embraced certification systems like the passive house standard, Energy Certification, and BREEAM, an equivalent to LEED.

The new construction sector has been important for guiding and building competence for a future of low carbon buildings; it has also facilitated customer and investor comparisons of building performance.

Regional approach and financial innovation are keys

While Scandinavian countries have pursued successful market transformation strategies for renewable thermal technologies, New England states are leading with green energy finance. Green Banks across the region are leveraging limited public funds and applying innovative financial instruments to mobilize private investments and overcome barriers to clean energy adoption. Including the measures of the utilities and energy agencies, the region has, at the ready, an extensive toolkit for financial innovation, such as leasing, community campaigns, first-loss loans, and Property Assessed Clean Energy (PACE) financing.

Opportunities to transform a practically non-existent market for renewable thermal technologies will arise through a coordinated regional effort. This can reduce barriers to entry, enhance competition, and reduce installation costs across states. The customer awareness of renewable thermal technologies is currently low, and must be improved to cultivate a regional industry. Unfamiliarity with the technologies creates skepticism about whether the technologies will actually perform as promised. These barriers can be better addressed on a regional level than on a state level. With these elements set in place, a market for renewable thermal technologies is ready to grow across New England, helping each state achieve their GHG emission reduction goals.

[1] Renewable thermal technologies (RTTs) harness renewable energy sources to provide heating and cooling services for space heating and cooling, domestic hot water, process heating, and cooking.

Photo: Alnön, Medelpad, Sweden | Credit: texturedJohn